Sold 16,000 shares of ComfortDelGro at $1.17 on 21 Mar.

Total loss including dividend is $5373.30 (-21.5%)

Reason for selling:

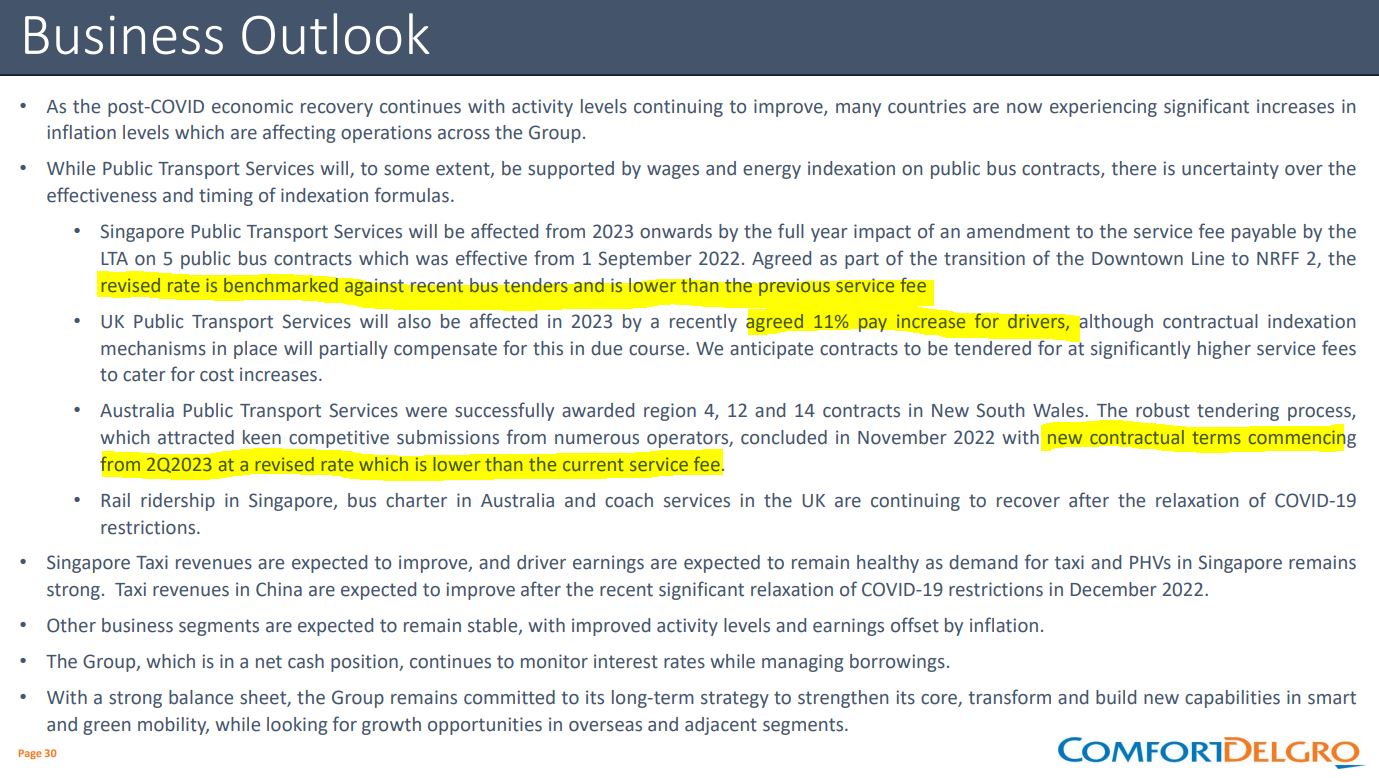

1) Share price remain weak

I am disappointed with CDG share price especially when the price post COVID is lower than pre COVID.

2) Weak Fundamental

Given the current Bus Contracting Model (BCM), I am expecting SBS Transit to further losing market share + lower margin.

The number of taxis on the roads are decreasing too.

Final dividend for FY22 is 16% lower than FY21 (1.76 cents vs 2.10 cents)

Inflation, rising wages, increasing interest rate and lower margin doesn't look good with CDG too.

1) Bad tenant news punished the share price

|

| https://sginvestors.io/analysts/research/2023/03/digital-core-reit-uob-kay-hian-research-2023-03-20 |

|

| https://sginvestors.io/analysts/research/2023/02/digital-core-reit-uob-kay-hian-research-2023-02-06 |

2) 52w low

IPO was priced at USD88 cents and it went to USD1.13 (52w high).

USD43cents is 51% lower than IPO price and 62% lower than 52w high.

I will term USD43cents as buying a fair company at wonderful price (Warren Buffet prefer buying Wonderful company at fair price).

3) Good USD exchange rate at this moment

4) Sponsor seem good

During Sungard bankruptcy incident, Sponsor step in to provide cash flow support.

Acquisition of 2 data centres was provided with 2 options. Given the market situation, a more favour options was selected.

5) Shares buyback

Digital Core Reit did 11 millions of shares buyback at average USD0.585 recently.

(NEW) Digital Core Reit started another phase of share buyback on 27 & 28 Mar.

6) Improving market rents

7) No loan expiring until 2025 + 75% fixed interest rate

Related post:

1) SOLD: AIMS APAC REIT & ADDED: Lendlease REIT

2) Added: ComfortDelGro (Oct 2021)

The dividends from Digital Core Reit is subject to withholding tax, right? I hesitated to invest in it since I reside in a country with no tax treaty with US.

ReplyDeleteHi

Deleteyou can refer to https://www.digitalcorereit.com/investor-relations/tax/default.aspx

I feel your pain regarding CDG but I feel that it has a more than fair chance of recovering to $1.50 in a year. As for DC Reit, I am wondering if retail investors are on a level playing field when it comes to information. All the info retail investors have (and most local analysts - who do not do independent research but just summarise company filings) are what the company gives you. So retail investors are competing against fund managers who can obtain higher quality information about the exact risks the tenants are facing, and also get better reads on the markets the REIT is operating in.

ReplyDeleteFinally, I see you are quoting UOB Kay HIan coverage. Just remember their Eagle HT coverage: https://research.sginvestors.io/2019/10/eagle-hospitality-trust-uob-kay-hian-research-2019-10-25.html

https://research.sginvestors.io/2019/08/eagle-hospitality-trust-uob-kay-hian-research-2019-08-29.html

Hi

Deletei am not sure if pain is the correct feeling but to me, is more toward disappointment with CDG. Reason because I was deciding between CDG vs SIA for post COVID recovery and I was expecting CDG to have a higher chance of faster recovery compare to SIA. When SIA shares roar back and resume dividend, CDG seem to be going downhill. In my Oct 2021 post here (https://compoundingdividendxdividend.blogspot.com/2021/10/added-comfortdelgro-oct-2021.html), I am expecting CDG to recover back abv $2 post COVID. What follow is more disappointment like AU IPO failed, fell out of STI, new foreign company bidding and remaining in Bus Contracting Model (BCM) is reducing market shares + profit margin and etc.

To be honest, i do not have fated in US related REIT for long term. Thus, I will likely sell off DC REIT when the share price is back to 50cents range (will not be greedy. Money in pocket is the safest as compare to paper gain) and rotate into a more stable stock which I can sleep soundly on. US related REIT majority ended up badly (below IPO price / delisting)